As we navigate through the second half of 2024, the European and UK economies are showing signs of recovery after facing significant challenges in recent years. The aftermath of the pandemic, energy crises, and persistent inflation have tested the resilience of these economies. However, recent data and forecasts suggest a cautiously optimistic outlook for the year ahead.

The first half of 2024 has brought mixed news for the European and UK economies.

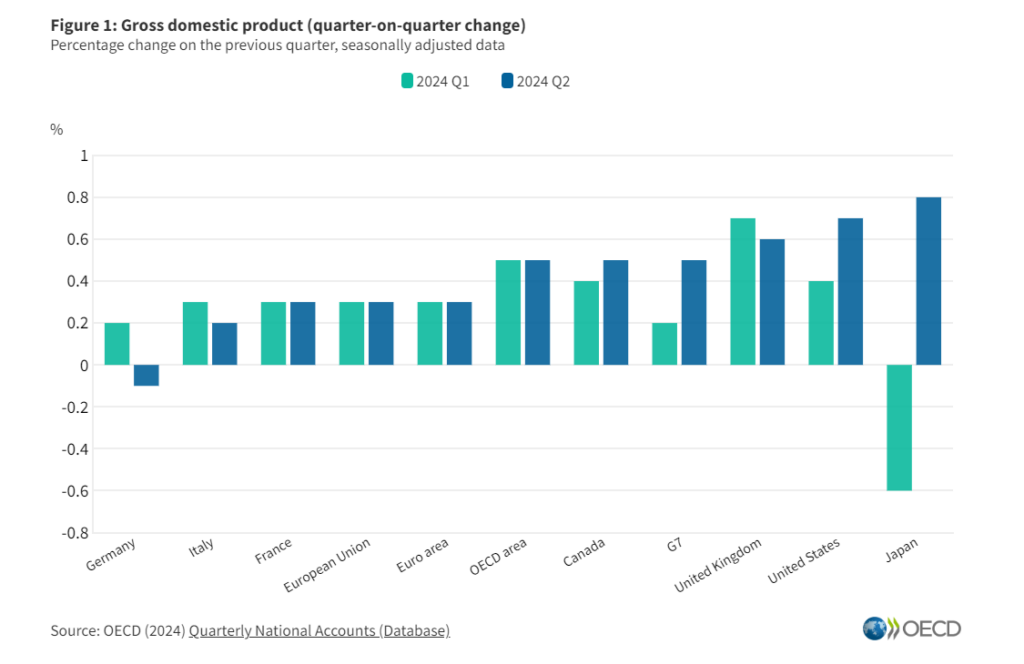

The euro zone economy expanded by 0.3% in both the first and second quarters of 2024, surpassing expectations and marking a clear break from the technical recession experienced in the latter half of 2023.

However, this growth has not been uniformed across the region. Germany, the euro zone’s largest economy, unexpectedly contracted by 0.1% in the second quarter, while countries like Latvia, Sweden, and Hungary also experienced GDP contractions.

The UK economy has shown more robust growth, expanding by 0.7% in the first quarter and 0.6% in the second quarter of 2024. However, growth flattened in June, partly due to heavy rain affecting retail sales and a doctor’s strike impacting healthcare activity.

Looking ahead, the Bank of England has revised its growth forecast for the UK upward to 1.25% for 2024, a significant improvement from the previous 0.5% projection. However, they anticipate slower growth in the latter half of the year, with 0.4% in Q3 and 0.2% in Q4.

For stock market enthusiasts, the outlook remains cautiously positive, with the STOXX 600 expected to reach 540 points by the end of 2024, implying a roughly 5% gain from August 2023 levels. The STOXX50E is projected to rise to 5,038, a 3.4% increase, while Germany’s DAX is forecasted to reach 19,000, representing a 3.1% gain.

The recovery continues to be uneven across sectors. While services are crucial to overall economic health, they face ongoing challenges in price normalisation.

Manufacturing, particularly in Germany, shows signs of weakness but has potential for improvement as global conditions enhance.

Several sectors are positioned for growth in 2024. Technology hardware and semiconductors are expected to benefit from ongoing digital transformation trends. The banking and insurance sectors may thrive in an environment of changing interest rates.

Utilities, particularly those focused on renewable energy, are likely to see growth as Europe continues its push towards sustainable energy solutions.

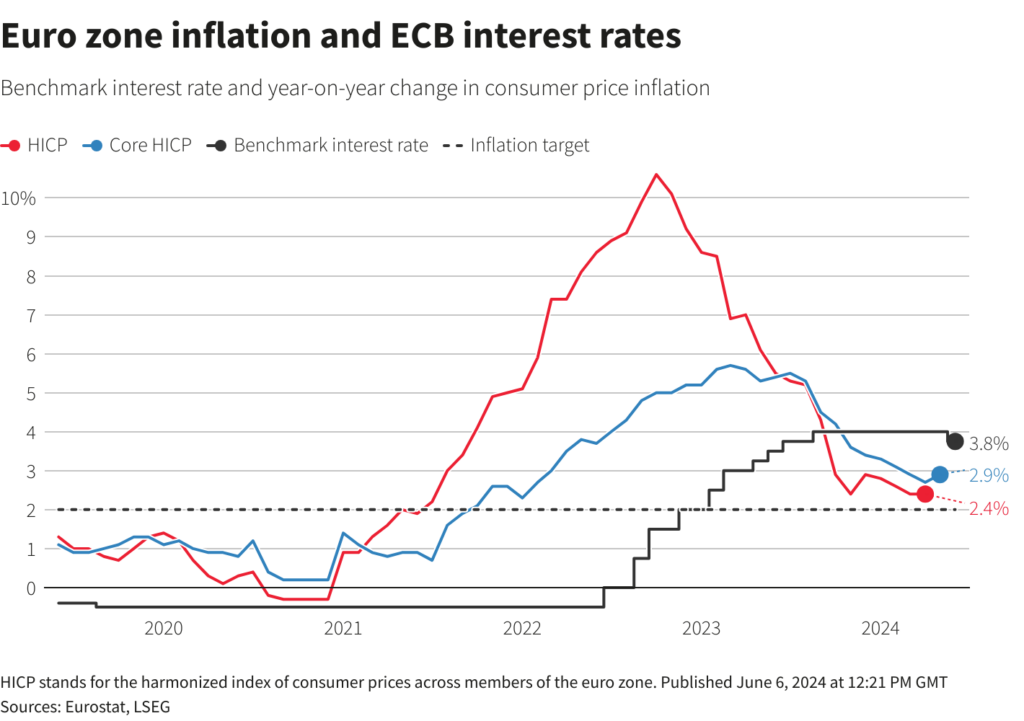

Central bank policies continue to play a crucial role in shaping the economic landscape in 2024, with inflation remaining a key focus prompting careful adjustments to monetary policy.

The European Central Bank (ECB) has already taken action this year, cutting its key interest rate from 4.00% to 3.75% on August 8. While the ECB recently kept rates steady, discussions are ongoing about a potential further cut in September, contingent on economic conditions and inflation trends.

Meanwhile, the Bank of England has been more aggressive in its approach, implementing two rate cuts thus far in 2024. The first reduction brought the rate down from 5.25% to 5.00%, with a second cut anticipated to lower it further to 4.75%. These moves align with the Bank’s revised growth forecasts and demonstrate a careful navigation of economic challenges.

These measured steps by both central banks reflect their delicate balancing act between supporting economic growth and keeping inflation in check. The policies are seen as essential to fostering economic recovery without reigniting inflation.

However, both institutions may continue to adopt a cautious approach due to persistent inflationary pressures, particularly in the services sector.

The possibility of additional adjustments later in the year remains open as central banks continue to closely monitor economic indicators. This ongoing vigilance underscores the complex nature of managing monetary policy in the current economic climate, where supporting growth must be balanced against the risk of overheating the economy.

Despite the positive outlook, several challenges and risks remain.

The uneven recovery across euro zone countries, particularly Germany’s contraction, highlights the fragility of the economic rebound.

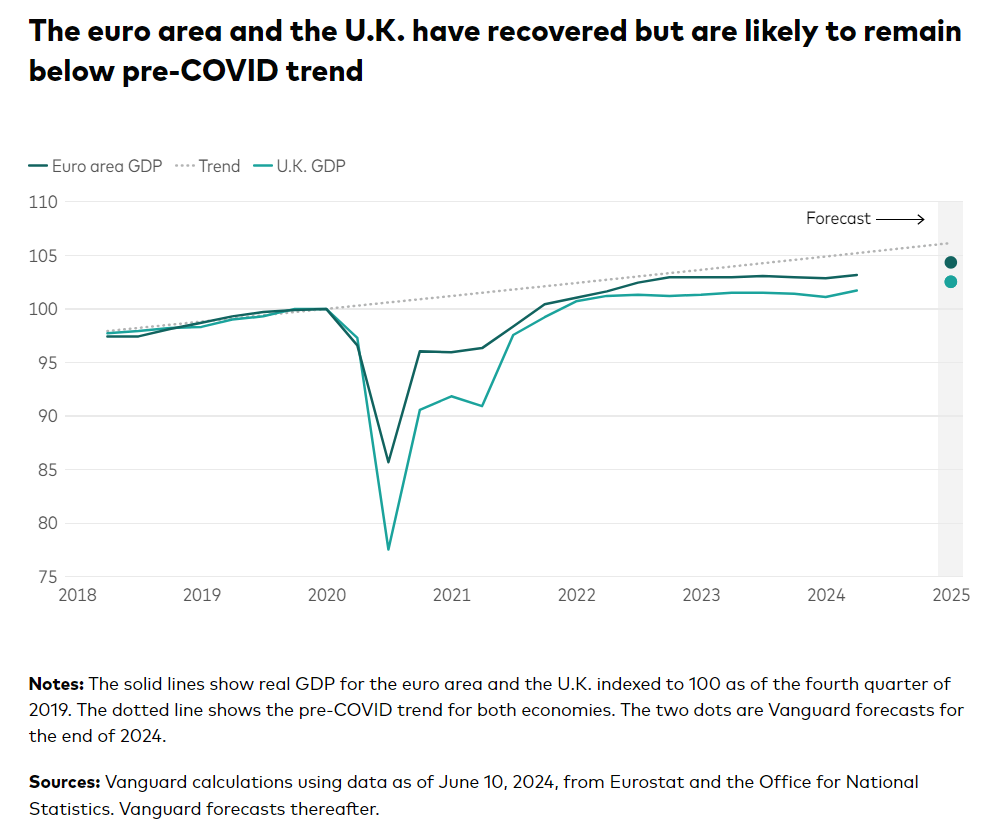

The UK’s long-term growth figures are concerning, with output per head still 0.8% lower than pre-pandemic levels and overall growth of just 2.3% since Q4 2019.

Business investment in the UK was 1.1% lower in Q2 2024 compared to the previous year, indicating ongoing uncertainties. Productivity issues, exacerbated by Brexit-related challenges, continue to weigh on the UK’s economic performance.

Geopolitical tensions and potential supply chain disruptions continue to pose risks to the recovery. Additionally, the moderation of wage growth, while helpful for inflation control, could impact consumer spending power.

For traders, 2024 presents a landscape of both opportunities and challenges. Sectors benefiting from structural shifts, such as technology and renewable energy, may offer growth potential.

The anticipated rate cuts could lead to broader market gains beyond just large-cap stocks, providing opportunities for diversification.

Traders should consider focusing on companies with strong fundamentals and those positioned to benefit from long-term trends like digital transformation and the transition to green energy.

The varying performance across euro zone countries also suggests opportunities in markets showing stronger growth, such as Ireland.

Seize these prospects by investing in EU and UK stocks with VT Markets, which also provides daily market analysis to help you make informed decisions and optimise your trading strategy.

As 2024 unfolds, the European and UK economies are showing signs of recovery, though progress is gradual and uneven. Economic growth, inflation control, and central bank policies will shape this recovery’s path.

Traders should stay informed and maintain a diversified strategy to navigate the markets effectively. The economic landscape remains complex, with varied performances across the euro zone and challenges in the UK. Continuous learning, careful analysis, and prudent risk management are crucial for success in this evolving environment.

![]()

Follow us on: