Midweek trading will be dominated by the highly anticipated Federal Reserve interest rate decision, setting the tone for global markets. Investors will also analyse economic data from China and the US, looking for further signs of economic momentum or slowdown. Expect heightened volatility across equities, bonds, and forex markets.

KEY INDICATORS

Federal Reserve interest rate decision & economic projections

The Fed will announce its policy decision, with markets closely watching for any changes in interest rates.

The FOMC economic projections (dot plot) will provide insights into the Fed’s future rate path.

Fed Chair Jerome Powell’s press conference will be key in shaping market sentiment.

China industrial production & retail sales (February)

Indicators of post-holiday economic activity and consumer demand.

A slowdown could trigger concerns about weaker global growth, affecting commodities and Asian markets.

US crude oil inventories

A key report for energy markets, influencing oil prices and inflation expectations.

MARKET MOVERS

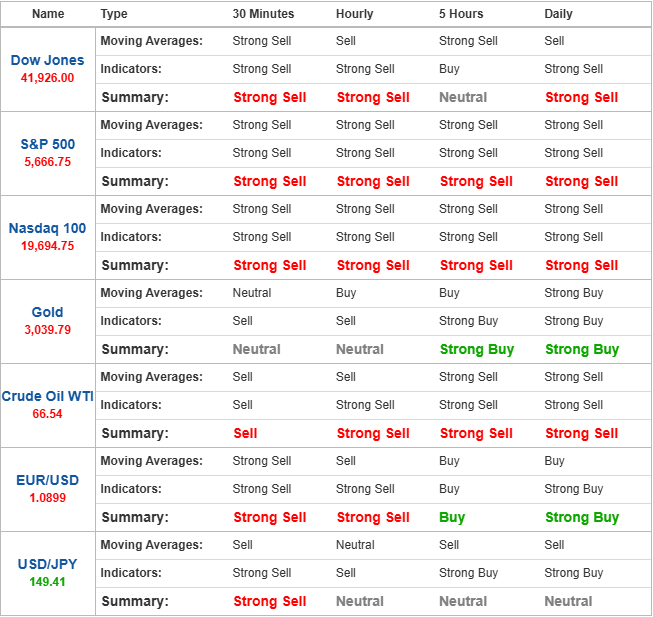

EUR/USD

Possible short preference

Short positions below 1.08759 with targets at 1.08554 and 1.08332 in extension.

Alternative scenario

Above 1.09211, look for further upside with 1.09412 and 1.09640 as targets.

The RSI calls for a new downleg.

Dollar weakens ahead of Fed meeting; euro gains ahead of German debt vote

The US dollar edged lower on Tuesday ahead of the start of the latest Federal Reserve meeting, while the euro gained ahead of an expected vote on Germany’s substantial stimulus plan.

At 9:00 AM GMT, the Dollar Index, which tracks the greenback against a basket of six other currencies, traded 0.1% lower at 102.890, remaining above last week’s five-month low.

In Europe, EUR/USD traded 0.3% higher at 1.0951, near its highest level since October, ahead of a scheduled parliamentary vote on Germany’s economic support package.

GBP/USD rose 0.1% to 1.3001, climbing above the 1.30 level for the first time since November.

The Bank of England is widely expected to keep interest rates unchanged on Thursday after inflation edged higher last month.

In Asia, USD/JPY climbed 0.3% to 149.70 ahead of the conclusion of the latest Bank of Japan meeting on Wednesday.

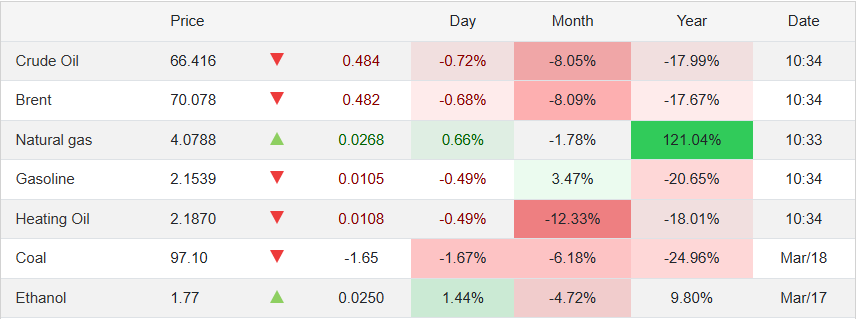

Oil slips after US-Russia agreement on 30-day energy ceasefire

Oil prices fell on Wednesday after Russia agreed to US President Donald Trump’s proposal that Moscow and Kyiv temporarily stop attacking each other’s energy infrastructure, which could lead to more Russian oil entering global markets.

Brent crude futures fell 23 cents, or 0.3%, to USD 70.33 a barrel by 07:30 GMT.

US West Texas Intermediate crude (WTI) was down 25 cents, or 0.4%, at USD 66.65.

Russian President Vladimir Putin agreed on Tuesday to stop attacking Ukrainian energy facilities but stopped short of endorsing a full 30-day ceasefire that Trump had hoped for.

US crude oil stocks data, meanwhile, painted a mixed picture, with crude stocks rising while fuel inventories fell.

Crude Oil WTI

Possible short preference

Short positions below 66.04, with targets at 65.81 and 65.46 in extension.

Alternative scenario

Above 66.55, look for further upside with 66.85 and 67.10 as targets.

The RSI advocates for further downside.

TODAY’S NEWS HEADLINES

Gold prices hit record high as haven demand grows ahead of Fed rate decision

Gold prices rose slightly to a record high in Asian trade on Wednesday, as safe-haven demand remained underpinned by renewed geopolitical ructions in the Middle East and concerns over trade tariffs.

Investors also remained largely risk-averse before the conclusion of a Federal Reserve meeting later on Wednesday, which is expected to offer more insight into the US economy.

Spot gold rose 0.1% to a record high of USD 3,039.0 an ounce.

Gold futures expiring in May rose 0.1% to a peak of USD 3,046.12 an ounce.

The Fed is widely expected to keep interest rates unchanged at 4.5% after the conclusion of its meeting later on Wednesday, amid persistent uncertainty over the US economy under Trump.

Platinum futures fell 0.4% to USD 1,016.90 an ounce.

Silver futures fell 0.5% to USD 34.55 an ounce.

Europe stocks close higher as Germany passes landmark fiscal package; Trump and Putin hold call

European markets closed higher on Tuesday, with investor focus on Germany’s historic debt reform deal and a closely watched phone call between US President Donald Trump and Russian leader Vladimir Putin.

European stocks on the Stoxx 600 index closed higher for a third straight session, adding another 0.59%, provisionally.

Germany’s DAX closed 1.03% higher.

France’s CAC 40 closed 0.5% higher.

The UK’s FTSE 100 ended 0.29% higher.

Asia-Pacific markets rise as Hong Kong tech stocks rally; Baidu shares pop 12%

Asia-Pacific markets rose on Tuesday, tracking gains on Wall Street, which ticked up after US retail sales data appeared to ease recession concerns.

Hong Kong’s Hang Seng Index led gains in Asia, rising 2.29% in its last hour on the back of strong moves in tech giants like Baidu, which was up 12.11% as of 3:45 p.m. local time.

Meanwhile, mainland China’s CSI 300 advanced 0.27% to end the day at 4,007.72.

The BOJ’s two-day meeting coincides with the US Federal Reserve, with the latter also expected to keep interest rates unchanged.

Japan’s benchmark Nikkei 225 ended the day 1.20% higher at 37,845.42.

Over in South Korea, the Kospi index closed flat at 2,612.34, while the small-cap Kosdaq added 0.27% to end at 745.54.

Australia’s S&P/ASX 200 ended the day flat at 7,860.40, paring gains from earlier in the session.