As the new trading week begins, investors are navigating a landscape shaped by recent market volatility following the introduction of new US tariffs. Today’s focus will be on inflation expectations, central bank commentary, and corporate earnings—all key drivers that could influence overall market sentiment.

KEY INDICATORS

US consumer inflation expectations (March)

The Federal Reserve Bank of New York is set to release its monthly survey, offering insights into consumers’ inflation expectations.

This data is crucial for gauging potential shifts in consumer behaviour and future monetary policy decisions.

Federal reserve speeches

Several Federal Reserve officials, including Patrick Harker and Raphael Bostic, are scheduled to speak.

Their remarks will be closely analysed for clues regarding the Fed’s stance on interest rates and the broader economic outlook.

International data releases

Japan: Reports on industrial production and capacity utilisation will offer insight into the health of Japan’s manufacturing sector.

Switzerland: The release of the Producer Price Index (PPI) will provide an update on inflationary pressures within the Swiss economy.

MARKET MOVERS

EUR/USD

Possible long preference

Long positions above 1.14198 with targets at 1.14401 and 1.14759 in extension.

Alternative scenario

Below 1.13638, look for further downside towards 1.13256 and 1.12815.

The RSI indicates further upside potential.

Asia FX weak with Chinese yuan down; dollar hits 3-year low amid brief tariff relief

Most Asian currencies weakened on Monday. The Chinese yuan remained fragile amid limited relief on US trade tariffs, while ongoing concerns over economic headwinds pushed the US dollar to a three-year low.

The Japanese yen outperformed, trading near its strongest level in six months as demand for safe havens remained high. The USD/JPY pair fell 0.3% to 143.09.

Chinese yuan dips as Beijing sets weak midpoint; trade data positive

The onshore USD/CNY pair rose 0.2% after another weak midpoint fix from the People’s Bank of China. The pair remained close to a 17-year high reached last week.

The PBOC has set a weaker midpoint in seven of the past eight sessions, with Beijing appearing to devalue the yuan to counteract steep US tariffs.

Last week, Trump hiked tariffs on China to a staggering 145%, with Beijing retaliating with 125% tariffs.

Gold prices dip from record highs amid some US tariff relief

Gold prices fell from record highs on Monday as risk appetite improved marginally following the US signalling some exemptions from steep trade tariffs against China, although sentiment remained largely cautious.

Spot gold fell 0.3% to USD 3,225.79/oz.

Gold futures expiring in June dropped 0.1% to USD 3,240.87/oz by 5:12 AM GMT.

Spot gold remained close to the record high of USD 3,245.69/oz reached last week.

Gold pressured by brief tariff relief as risk appetite recovers

Losses in gold came amid gains in risk-driven markets, with Asian stocks mostly rallying on Monday. US stock index futures also rose during Asian trading hours.

Beijing announced 125% retaliatory tariffs against the US in response to Trump’s latest move, showing little intention of backing down.

Platinum futures rose 0.8% to USD 951.90/oz.

Silver futures fell 0.3% to USD 31.827/oz.

Among industrial metals, copper futures on the London Metal Exchange steadied at USD 9,152.90 per tonne.

XAU/USD

Possible long preference

Long positions above 3,235.41 with targets at 3,246.42 and 3,262.65 in extension.

Alternative scenario

Below 3,209.91, expect further downside towards 3,194.27 and 3,176.88.

While further consolidation cannot be ruled out, it is expected to remain limited.

TODAY’S NEWS HEADLINES

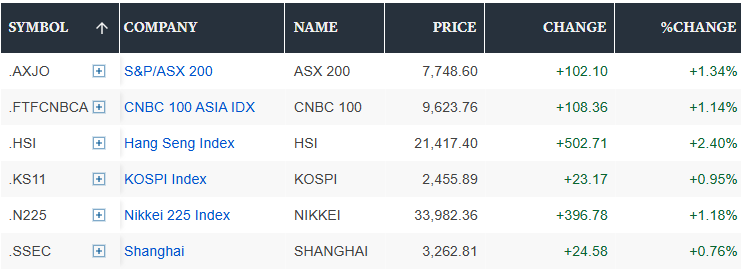

Hong Kong shares rise over 2% to lead gains in Asia after Trump pauses tariffs on consumer electronics

Asia-Pacific markets climbed on Monday as US President Donald Trump paused tariffs on some consumer electronics, boosting risk sentiment.

Hong Kong stocks led gains in the region, with the Hang Seng Index ending the day 2.4% higher at 21,417.40.

The Hang Seng Tech Index rose 2.34% to 5,015.12.

Mainland China’s CSI 300 increased 0.23% to close at 3,759.14.

Japan’s benchmark Nikkei 225 ended the day 1.18% higher at 33,982.36.

In South Korea, the Kospi index added 0.95% to close at 2,455.89.

Meanwhile, Australia’s S&P/ASX 200 rose 1.34% to close at 7,748.60.

Japan’s Nikkei jumps over 9% to lead gains in Asia after Trump pauses tariffs

Asia-Pacific markets rose on Thursday, following Wall Street’s biggest burst of buying since 2008, after US President Donald Trump announced a 90-day pause on higher tariffs for all nations except China.

US futures fell, even as Trump’s pledge to pause tariffs on some trading partners for 90 days spurred a massive surge on Wall Street.

Overnight in the US, the broad-based S&P 500 skyrocketed 9.52% to close at 5,456.90 — its biggest one-day gain since 2008.

European markets close lower as traders brace for Trump’s tariff plans

European markets closed lower on Wednesday as global traders braced themselves for a raft of fresh trade tariffs due to be announced by US President Donald Trump’s administration.

After rebounding on Tuesday, the regional Stoxx 600 index closed down 0.6%. Most sectors recorded declines, though retail and utilities stocks posted slight gains.

Germany’s DAX dropped 0.7%, while France’s CAC 40 was down 0.2%.