As we enter the week of 31 March to 4 April 2025, global markets face rising uncertainty, with US tariff announcements, inflation data, and geopolitical risks set to drive volatility across equities, forex, and commodities. Traders are bracing for potential shifts in market sentiment as these events unfold.

KEY INDICATORS

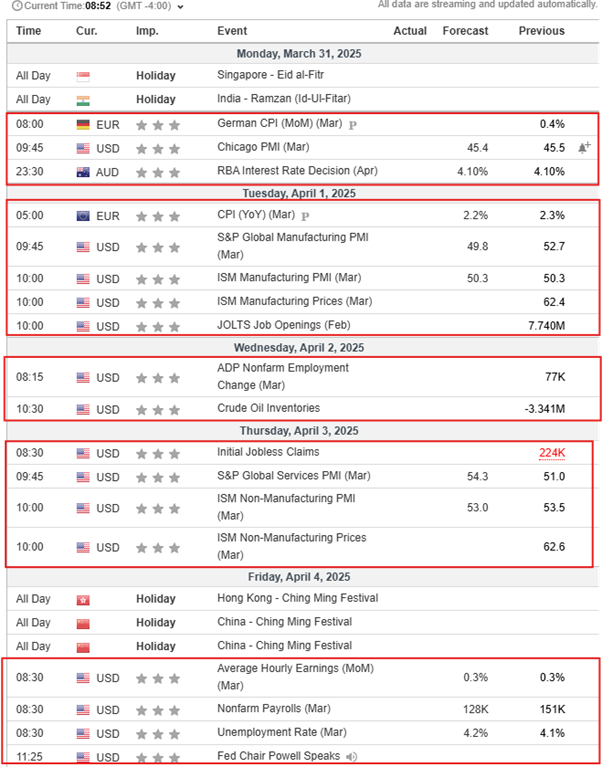

US tariff announcements: On 2 April, President Trump is set to unveil new “reciprocal tariffs,” possibly including a 25% duty on imported vehicles, fuelling market uncertainty.

Economic data: US jobs report (4 April): Expected to show slower job growth, highlighting economic fragility amid trade tensions.

Inflation: PCE price index rose 2.5% YoY in February, with a 0.3% MoM increase.

Market performance: The S&P 500 is down nearly 7% from its February peak, with tech stocks leading declines.

International developments: India plans to raise 8 trillion rupees (USD 93.34B) via bond sales to manage its 4.4% fiscal deficit.

Australia: The RBA is expected to hold rates steady, though markets anticipate a cut in May.

Investor sentiment: Rising volatility due to trade policy uncertainty, economic data, and geopolitical risks. Caution is advised.

MARKET MOVERS

XAU/USD

The price action has reached a new all-time high of 3085.9.

Trading volume is on the rise.

The overall trend continues to be bullish.

Given the current levels, the risk/reward ratio for entering a buy position is not favourable.

We expect a brief pullback before any further movement.

US dollar (USD): The dollar edged lower as investors remained cautious amid uncertainty over US tariffs and ahead of key US economic data.

Euro (EUR): The euro is on track for its most significant quarterly gain in over a year, bolstered by optimism surrounding peace prospects in Ukraine and rising German yields. Market participants are closely monitoring upcoming inflation figures from France and Spain, as softer readings could influence the euro’s trajectory.

Japanese yen (JPY): The yen has strengthened, reflecting its status as a safe-haven currency amid global trade uncertainties. Additionally, higher-than-expected Tokyo inflation data for March, at 2.4% versus the anticipated 2.2%, supports the case for potential monetary policy adjustments by the Bank of Japan.

British pound (GBP): Sterling remains steady, maintaining a 3.5% gain for the year. The UK’s economic data, including marginal growth in the fourth quarter and an unexpected rebound in retail sales, has provided support to the pound.

Commodities and stocks

US stock market: US stock futures are under pressure as investors grapple with the prospect of more tariffs from the Trump administration and await key inflation data. The Personal Consumption Expenditures (PCE) Price Index, a key inflation measure, rose 2.5% in February on an annual basis, aligning with expectations. On a monthly basis, the index increased by 0.3%.

Gold: Gold prices have surged to a record high, surpassing USD 3,075 per ounce. This increase is driven by investors seeking safe-haven assets amid escalating trade war concerns and economic uncertainties.

Oil: Oil prices are trading nearly flat, with volatility in the energy commodities market remaining very low.

Copper: Copper prices in London have declined for a third consecutive day, sliding further below USD 10,000 a ton, impacted by the tariff threats.

European and Asian markets: European markets are experiencing small declines, while Asian markets have faced larger drops. Japan’s Nikkei and South Korea’s benchmark index both dropped by around 2% due to concerns over auto tariffs and inflation.

Market outlook: Investors are closely watching the release of the US Personal Consumption Expenditures (PCE) inflation data, as it could provide further insights into the Federal Reserve’s monetary policy direction. Additionally, President Donald Trump’s announcement of new “reciprocal tariffs” is generating apprehension, especially with hints at a 25% duty on imported vehicles.

Overall: Global markets are navigating a complex landscape shaped by trade policy developments, economic data releases, and shifting investor sentiments.

Asian session updates

Asian financial markets experienced notable movements influenced by recent geopolitical developments and economic data releases.

Japan: The Nikkei 225 index declined nearly 2%, led by sharp drops in major automakers such as Toyota and Honda. This downturn is attributed to investor concerns over the US administration’s decision to implement a 25% tariff on auto imports, effective next week.

Hong Kong: The Hang Seng index declined by 0.6% as traders awaited further clarity on US tariff plans, particularly concerning China.

China: The Shanghai Composite Index decreased by 0.7%, reflecting investor caution amid ongoing trade tensions and awaiting further policy signals.

Gold: Gold prices reached a record high, surpassing USD 3,079.5 per ounce, as investors sought safe-haven assets amid escalating trade war concerns. The metal has gained more than 17% in the first quarter, marking its best quarterly performance since 1986.

Oil: Oil prices experienced slight declines due to concerns over the impact of new tariffs on the global economy. Brent crude futures were 0.24% lower at USD 73.85 a barrel, while US West Texas Intermediate crude futures decreased by 0.27% to USD 69.73.

US dollar: The dollar remained steady ahead of the release of the US Personal Consumption Expenditures (PCE) inflation data.

Japanese yen: The yen strengthened to 150.675 per dollar.