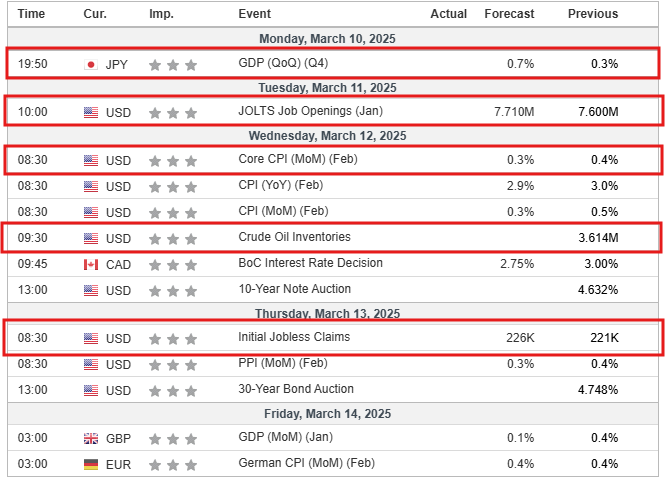

This week, global markets will focus on key economic data releases, central bank decisions, and geopolitical developments. With inflation trends, employment reports, and monetary policy updates on the agenda, investors should prepare for potential volatility across equities, forex, and commodities.

KEY INDICATORS

Monday, 10 March:

Japan GDP (Q4 2024 Final Estimate) – A key indicator of Japan’s economic health, impacting the JPY and regional markets.

UK Industrial Production (January) – Provides insights into Britain’s economic momentum.

Tuesday, 11 March:

US Inflation Report (February CPI) – A crucial release for Federal Reserve policy expectations. Markets will react strongly to any deviations from forecasts.

Germany ZEW Economic Sentiment Index – A leading indicator of economic confidence in the Eurozone’s largest economy.

Thursday, 13 March:

European Central Bank (ECB) Interest Rate Decision – The ECB’s stance on inflation and future rate moves will be closely watched.

US Producer Price Index (PPI, February) – Inflationary pressures at the wholesale level could influence Fed policy expectations.

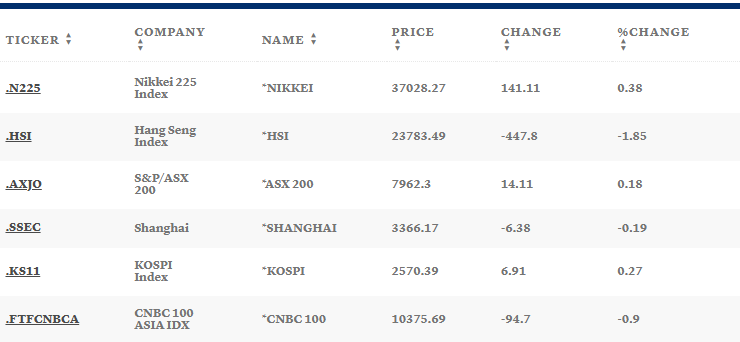

Asia-Pacific markets mixed after volatile trading week

Asia-Pacific markets were mixed on Monday after a volatile trading week around the world.

US stocks — which are expected to open lower on Monday — have been on a roller-coaster ride since the start of the month due to uncertainty surrounding US President Donald Trump’s tariff policies, and their impact on the superpower’s growth and inflation.

Japan’s benchmark Nikkei 225 led gains in Asia, rising 0.38% in choppy trade, to end the day at 37,028.

The broader Topix index, meanwhile, fell 0.29% to close at 2,700, paring earlier gains.

The country’s cash earnings rose 2.8% year-on-year in January, slowing from December’s revised 4.4% climb.

South Korea’s Kospi added 0.27%, to end the day at 2,570, while the small-cap Kosdaq fell 0.26% to 725.

Australia’s S&P/ASX 200 rose 0.18% to end the day at 7,962, after closing at a six-month high in its previous session.

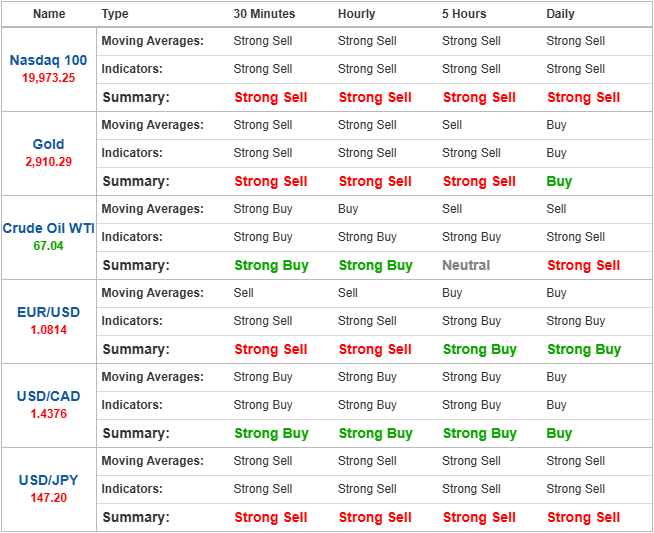

Japanese yen bulls retain control amid bets for more BoJ rate hikes

The Japanese yen continues to draw support from bets for more BoJ rate hikes.

The narrowing US-Japan rate differential further benefits the lower-yielding JPY.

Expectations that the Fed will resume its rate-cutting cycle undermine the USD.

The Japanese yen remains on the front foot against the USD amid divergent BoJ-Fed expectations.

MARKET MOVERS

USD/JPY

Potential short preference Short positions below 147.005 with targets at 146.699 & 146.300 in extension. Alternative scenario Above 147.504 look for further upside with 147.795 & 148.156 as targets. The RSI is bearish and calls for further decline.

USD/CAD

Potential short preference Short positions below 1.43595 with targets at 1.43423 & 1.43157 in extension. Alternative scenario Above 1.43882 look for further upside with 1.44088 & 1.44214 as targets. The RSI is mixed with a bearish bias.

Technical indicators

Nasdaq 100

The short preference Short positions below 19860.54 with targets at 19742.88 & 19614.90 in extension. Alternative scenario Above 20071.08 look for further upside with 20135.07 & 20227.96 as targets. The RSI is mixed to bearish.

NEWS HEADLINES

European markets reverse course to trade lower as volatility persists

European markets were trading lower on Monday, erasing gains seen earlier in the session to continue the volatility seen in global markets last week.

The pan-European Stoxx 600 was 0.3% lower at 9:26 a.m. London time, with all major bourses in negative territory.

Germany’s Dax was 0.5% lower, after edging higher during early morning deals.

China bond yields jump to three-month highs as investors pare rate cut expectations

China’s sovereign bond yields hit their highest levels this year, as investors trimmed holdings on bets that additional fiscal spending will boost growth and push back interest rate cuts.

Yields on China’s 10-year government bond, which moves inversely to prices, gained over 10 basis points on Monday to hit 1.865%, their highest level this year.

The sell-off in bonds followed a rally in the Chinese offshore stock market, signalling a shift of liquidity toward riskier assets.

Yields on 30-year sovereign bonds climbed above the key psychological level of 2% to reach 2.030% on Monday, while yields on the one-year note also gained 10 basis points to hit 1.643%. By 1 p.m. in Beijing, yields had pared some gains.

Stock futures fall on Monday morning after S&P 500’s worst week since September

Stock futures moved lower on Monday morning ahead of a packed week of economic data, with investors smarting from losses in early March.

Futures for the S&P 500 fell 0.42%.

Nasdaq 100 futures dropped 0.53%.

Futures tied to the Dow Jones Industrial Average slipped 144 points, or 0.34%.

Last week, the S&P 500 fell 3.10% for its worst weekly mark since September.

The Dow fell 2.37%.

The Nasdaq Composite shed 3.45%.

On the inflation front, the February consumer price index release is slated for Wednesday, followed by the producer price index on Thursday.