During the week of 28 April to 2 May 2025, several key economic indicators and events are anticipated to influence financial markets, including crucial data on US labour market conditions, inflation, and GDP growth. Central bank decisions and global trade developments are also expected to drive volatility, with market participants closely monitoring policy shifts and economic outlooks from both the Federal Reserve and the European Central Bank.

KEY INDICATORS

Global trade and tariff developments

US media report that Trump is considering a tiered tariff system on China, according to CCTV.

The White House says Trump’s stance on China tariffs remains unchanged.

South Korea’s finance minister says a consensus has been reached with the US on tariffs, non-tariff barriers, economic security, investment cooperation, and monetary policy.

The White House NEC director says top-level tax negotiators are scheduled to meet next week.

Central bank signals and economic outlooks

Fed’s Harker says the central bank may cut rates in June if economic data become clearer.

Fed’s Waller says clarity on the economic impact of tariffs may emerge by July and rate cuts could follow if unemployment rises.

Atlanta Fed GDPNow estimates Q1 US GDP growth at -2.5%.

Fed’s Kashkari says constant announcements from Washington pose challenges for both policymakers and the public.

ECB Governing Council member Rehn says the central bank should not rule out the possibility of deeper rate cuts.

The ECB will hold a strategy meeting on 6–7 May to discuss a potential shift towards more flexible policies.

Economic data from the US and Germany

US initial jobless claims for the week ending 19 April were 222,000, in line with expectations.

US durable goods orders rose 9.2% month-on-month in March, the largest increase since July 2024.

The German government now forecasts 0% economic growth in 2025, down from a previous projection of +0.3%.

Germany’s inflation is projected to fall to 2.0% in 2025 and 1.9% in 2026.

MARKET MOVERS

XAU/USD

Although the bulls are in control, the stalling positive momentum indicates a turnaround is possible.

While the bulls maintain control, fading upside momentum suggests a potential reversal.

A corrective move lower is anticipated.

A short-term bounce may occur before the next leg down.

The US dollar eased after a two-day rebound, with the Dollar Index retreating to 99.30.

EUR/USD gained 80 pips, advancing to 1.1393.

USD/JPY declined 87 pips, settling at 142.57.

GBP/USD climbed 89 pips to 1.3344.

AUD/USD strengthened by 50 pips, reaching 0.6409.

USD/CHF edged down 39 pips to 0.8269.

USD/CAD slipped 37 pips, trading at 1.3843.

US stocks soar on strong earnings and economic data

US stocks rallied for a third consecutive session on Thursday.

Dow Jones rose 486 points (+1.23%) to 40,093.

S&P 500 gained 108 points (+2.03%) to 5,484.

Nasdaq 100 jumped 521 points (+2.79%) to 19,214.

Nvidia, Tesla, Microsoft, and Amazon each gained over 3%.

Alphabet rose 2.53% and surged over 4% after-hours following strong earnings and a USD 70bn buyback plan.

The US 10-year yield fell 7 basis points to 4.313%, continuing its decline.

Durable goods orders surged 9.2% in March (vs. +1.7% expected).

Existing home sales dropped 5.9% (vs. -1.9% expected), marking the steepest decline since late 2022.

European stock indices edged higher: DAX +0.47%, CAC 40 +0.27%, FTSE 100 +0.05%.

WTI crude rose USD 0.52 to USD 62.79/bbl.

Market reacts to Japan’s inflation and global moves

During the Asian session, USD/JPY rebounded to 142.95 after Tokyo CPI rose 3.5% year-on-year in April (vs. 3.1% expected).

EUR/USD pulled back to 1.1347, while GBP/USD slipped to 1.3305.

Gold rebounded USD 60 (+1.85%) to USD 3,349/oz, ending a two-day decline and holding steady around USD 3,348.

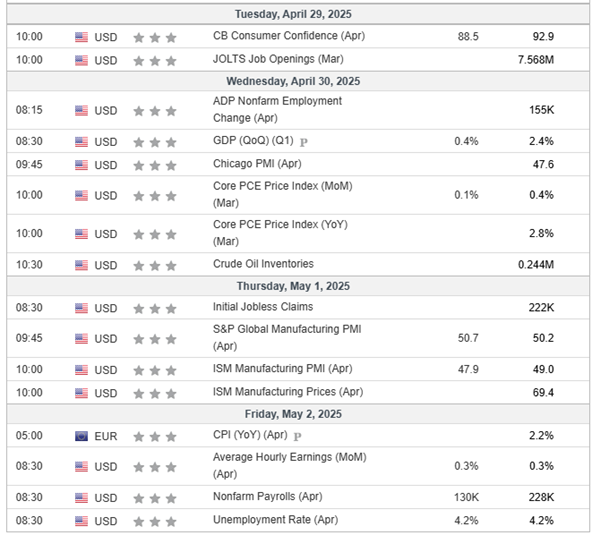

KEY ECONOMIC EVENTS

Traders should brace for a data-heavy week ahead, with key releases including US non-farm payrolls, ISM manufacturing and services PMIs, and Eurozone inflation figures—all of which could significantly shape market expectations around central bank policy moves. Stay alert for volatility, especially around labour market and inflation-related surprises.

Tuesday, 29 April

German Preliminary CPI (MoM): A critical indicator for assessing inflation trends in the Eurozone’s largest economy.

US CB Consumer Confidence: Provides insights into consumer sentiment and potential spending behaviours.

Wednesday, 30 April

US ADP Non-Farm Employment change: Offers an early look at private sector employment trends ahead of the official jobs report.

US Advance GDP (Q1): Initial estimate of economic growth for the first quarter, influencing market expectations.

US Core PCE Price Index (MoM): The Federal Reserve’s preferred inflation measure, critical for monetary policy decisions.

Bank of Japan monetary policy meeting (Day 1): Commencement of the BOJ’s two-day policy meeting, with potential implications for global markets.

Thursday, 1 May

Bank of Japan interest rate decision: Conclusion of the BOJ’s policy meeting, with announcements on interest rates and economic forecasts.

US ISM Manufacturing PMI: Measures manufacturing sector activity, a key indicator of economic health.

US Unemployment Claims: Weekly data on jobless claims, providing insights into labour market conditions.

Bank holidays: Markets in China, Switzerland, France, Germany, and Italy will be closed, potentially leading to reduced liquidity.

Friday, 2 May

US Non-Farm Payrolls (April): The most anticipated labour market report, influencing Federal Reserve policy and market sentiment.

US Unemployment Rate: Provides the overall unemployment figure, complementing the NFP data.

US Average Hourly Earnings (MoM): Indicates wage growth, a key factor in inflation and consumer spending.

Eurozone Flash CPI (YoY): Preliminary inflation data for the Eurozone, essential for ECB policy considerations.

Final Manufacturing PMI (Eurozone & UK): Final readings on manufacturing activity, reflecting economic momentum.