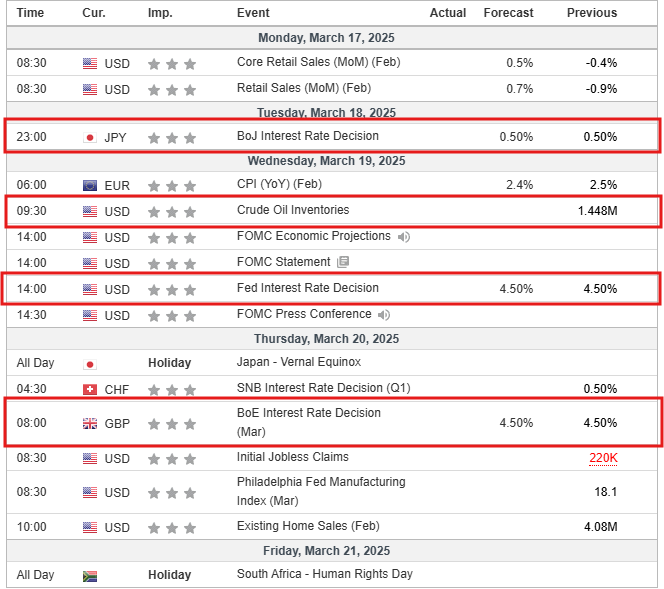

Next week, global markets will be driven by key central bank decisions, economic data releases, and geopolitical developments. Investors will focus on the Federal Reserve’s policy outlook, inflation reports, and economic activity indicators from major economies. Volatility is expected across equities, forex, and commodities as markets respond to these crucial events.

KEY INDICATORS

Monday, 17 March

Eurozone final CPI (February) – Confirms inflation trends ahead of the ECB’s next policy move.

US NAHB housing market index (March) – Provides insights into the health of the US real estate sector.

Wednesday, 19 March

Federal Reserve interest rate decision & economic projections – Markets will focus on Fed Chair Powell’s comments for signals on future rate moves.

Market reaction – Potential impact on equities, bonds, and the US dollar.

Thursday, 20 March

Bank of England (BoE) interest rate decision – The BoE’s stance on inflation and potential rate cuts will be closely watched.

US jobless claims & existing home sales (February) – Labour market trends and housing market strength will influence market sentiment.

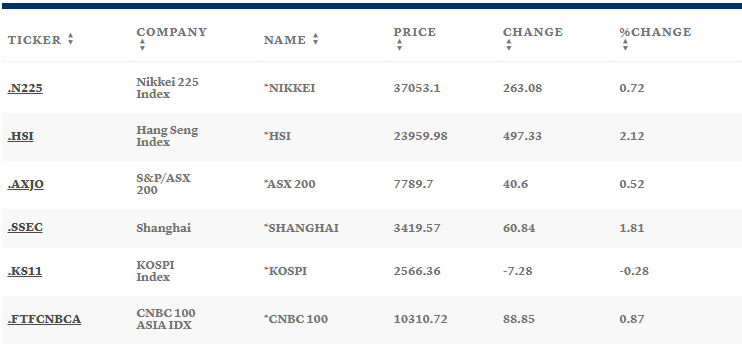

Chinese stocks close at three-month high, leading gains in Asia, despite fall on Wall Street

Asia-Pacific markets mostly rose on Friday, despite a plunge in all three benchmarks in the US over the previous session amid concern about President Donald Trump’s tariff plans.

Mainland China’s CSI 300 led gains in Asia, rising 2.43% to end the day at a three-month high of 4,006.56. This follows stronger movements in the healthcare, consumer cyclicals, and non-cyclicals sectors.

Hong Kong’s Hang Seng Index rose 2.12% to end the day at 23,959.98.

In Japan, the benchmark Nikkei 225 ended the day 0.72% higher at 37,053.10, while the broader Topix index rose 0.65% to 2,715.85.

South Korea’s Kospi index lost 0.28% to close at 2,566.36, while the small-cap Kosdaq advanced 1.59% to 734.26.

Australia’s S&P/ASX 200 ended the trading day 0.52% higher at 7,789.70.

Dollar edges higher ahead of Michigan sentiment data; euro slips

The US dollar edged higher on Friday amid growing expectations that a government shutdown can be averted, while the euro handed back recent gains amid concerns that a global trade war risks a sharp regional economic downturn.

At 9:15 AM GMT, the Dollar Index, which tracks the greenback against a basket of six other currencies, traded 0.2% higher at 103.982, moving further away from Tuesday’s trough of 103.21, its lowest since mid-October.

The greenback has fallen more than 4% so far this year, retreating from the six-month high seen in January, as the uncertainty surrounding the Trump administration’s trade policies raised fears of a US recession.

In Europe, EUR/USD traded marginally lower at 1.0851, sliding further from Tuesday’s five-month peak as the EU-US trade spat rattled traders and after Germany struggled to pass a massive spending proposal.

MARKET MOVERS

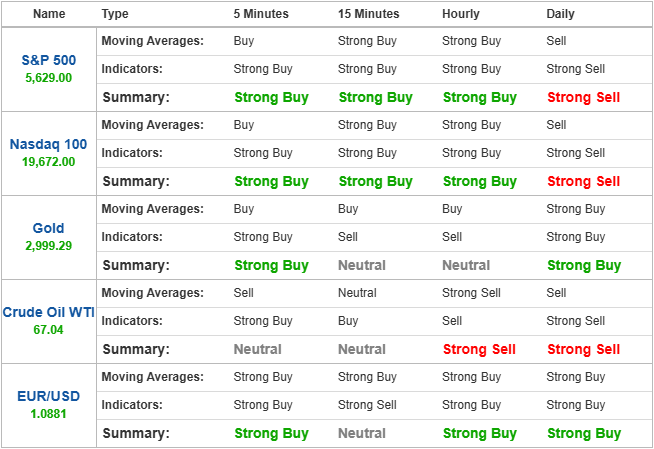

Crude Oil WTI

Potential short preference Short positions below 66.56 with targets at 66.16 & 65.48 in extension. Alternative scenario Above 67.42 look for further upside with 67.88 & 68.48 as targets. The RSI is below its neutrality area at 50%

XAU/USD

Potential long preference Long positions above 2997.21 with targets at 3005.29 & 3016.05 in extension. Alternative scenario Below 2978.38 look for further downside with 2962.38 & 2945.51 as targets. The next resistances are at 3005.29 and then at 3016.05.

Technical indicators

DAX40

The long preference Long positions above 23014.0 with targets at 23105.6 & 23210.7 in extension. Alternative scenario Below 22888.8 look for further downside with 22785.9 & 22631.7 as targets. A support base at 22785.9 has formed and has allowed for a temporary stabilisation.

NEWS HEADLINES

US stocks climb with government shutdown likely averted, consumer sentiment slips

US stocks rose on Friday, bouncing back at the end of the week after the bellwether S&P 500 index slipped into correction territory on concerns over an escalating trade war and potential recession.

At 1:45 PM GMT, the Dow Jones Industrial Average traded 270 points, or 0.7%, higher.

The S&P 500 index rose 68 points, or 1.2%.

The NASDAQ Composite gained 295 points, or 1.7%.

The S&P 500 closed 1.4% lower on Thursday, entering correction territory, which is typically defined as a 10% fall from a recent peak.

The Dow is on track for its second straight losing week and its worst weekly decline since June 2022. This would be the fourth consecutive negative week for the S&P 500 and Nasdaq.

Oil prices set to end the week stable as investors mull path to Ukraine ceasefire

Oil prices edged higher on Friday after a more than 1% loss in the previous session, as investors weighed the diminishing prospects of a quick end to the Ukraine war that could bring more Russian energy supplies back to Western markets.

Brent crude futures were up 36 cents, or 0.52%, to USD 70.24 per barrel at 3:30 PM GMT, after settling 1.5% lower in the previous session.

US West Texas Intermediate (WTI) crude was at USD 66.94 per barrel, up 39 cents, or 0.59%, after closing 1.7% lower on Thursday.

Prices are set to end the week relatively stable, with Brent settling at USD 70.36 and WTI at USD 67.04 last Friday.

Gold prices break USD 3,000/oz level, new record high on tariff fears

Gold prices surged to an all-time high on Friday, breaking through the key USD 3,000 per ounce level, supported by US President Donald Trump’s fresh tariff threats, while soft US inflation data further lifted sentiment.

At 12:30 AM GMT, spot gold was up 0.6% at USD 3,009.11 per ounce, after reaching a fresh record high of USD 3,017.11 earlier in the session.

Gold futures expiring in April gained 0.3% to USD 2,998.78 per ounce.

Platinum futures rose 0.9% to USD 1,015.00 per ounce.

Silver futures gained 1.3% to USD 34.755 per ounce.