As global markets head into the second week of May, investors will be closely watching a packed schedule of central bank decisions, key economic data releases, and geopolitical developments.

With US and European monetary policy moves, trade tensions, and oil market dynamics in focus, the week ahead promises important signals for growth, inflation, and market sentiment worldwide. Here’s a snapshot of the notable events shaping the week.

KEY INDICATORS

Central bank decisions in focus

US Federal Reserve (6–7 May): The Federal Reserve is expected to maintain current interest rates at its upcoming meeting, despite political pressure and a recent GDP contraction. Markets are hopeful for potential rate cuts starting in June, especially if inflation continues to ease.

Bank of England (8 May): The Bank of England is anticipated to implement a 25-basis point rate cut, marking its second reduction this year. This move aims to address low inflation and sluggish wage growth.

Key economic indicators

Monday, 5 May: US ISM Services PMI and S&P Global Services PMI for April.

Tuesday, 6 May: US trade balance data for March.

Wednesday, 7 May: Federal Reserve interest rate decision and press conference.

Thursday, 8 May: US initial jobless claims and labour productivity figures.

Friday, 9 May: US wholesale inventories and sales data.

Global market dynamics

Trade tensions and market sentiment: Recent US tariffs have disrupted global trade, leading to decreased container shipments and concerns over a potential recession. While some progress has been made in trade negotiations, uncertainties remain.

Oil market outlook: Oil prices have seen modest gains amid expectations that OPEC+ may increase supply. However, the market remains cautious due to ongoing trade tensions and economic uncertainties.

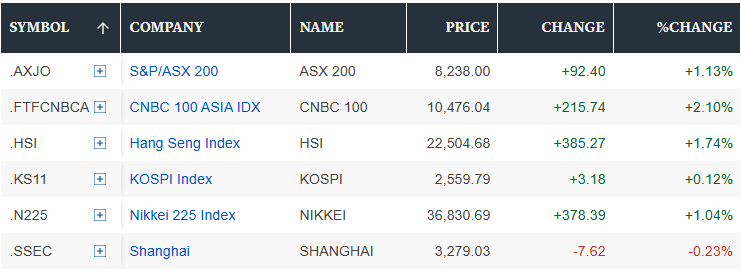

Japanese and Australian stocks rise as Bank of Japan holds rates and most Asian markets close for holiday

Japanese and Australian stocks rose in choppy trade, supported by a steady monetary policy stance from the Bank of Japan.

Japan’s Nikkei 225 gained 1.13% to close at 36,452.30, while the Topix index rose 0.46% to 2,679.44.

The Bank of Japan held interest rates unchanged at 0.5% in a unanimous decision.

The Japanese yen weakened by 1.06%, trading at 144.58 per US dollar.

Australia’s S&P/ASX 200 ended the session 0.24% higher at 8,145.60.

Several Asia-Pacific markets, including China and South Korea, were closed for the Labour Day holiday.

Asia-Pacific markets rose after China said that it was evaluating possible trade talks with the US. Markets in the region also trailed gains on Wall Street after all three key benchmarks advanced overnight on optimism that a slowdown in the global economy will not impede the progress of developments in artificial intelligence.

MARKET MOVERS

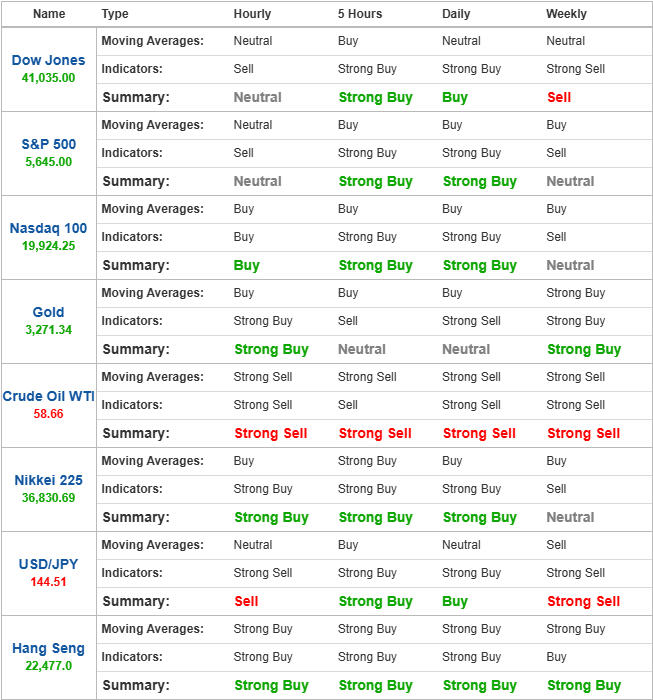

Crude Oil WTI

Potential long preference

Long positions above 58.96 with targets at 59.42 & 59.83 in extension.

Alternative scenario

Below 58.22 look for further downside with 57.88 & 57.04 as targets.

Even though a continuation of the consolidation cannot be ruled out, its extent should be limited.

Nikkei 225

Potential short preference

Long positions above 36780 with targets at 36900 & 37030 in extension.

Alternative scenario

Below 36596 look for further downside with 36413 & 36200 as targets.

The RSI advocates for further advance.

Nasdaq 100

The long preference

Long positions above 19895.90 with targets at 19976.86 & 20083.84 in extension.

Alternative scenario

Below 19765.79 look for further downside with 19679.05 & 19572.07 as targets.

As long as 19765.79 is support, look for choppy price action with a bullish bias.

NEWS HEADLINES

Euro zone inflation unchanged at 2.2% in April, leaving path open for further ECB interest rate cuts

Euro zone inflation remained unchanged at 2.2% in April, according to flash data from statistics agency Eurostat.

Economists polled by Reuters had expected a reading of 2.1% in April, down slightly from March’s 2.2%.

Both core and services inflation re-accelerated compared to March’s readings.

Core inflation — which excludes more volatile food, energy, alcohol and tobacco prices — accelerated to 2.7% from 2.4% in March.

The closely watched services inflation measure also picked up, coming in at 3.9%, up from 3.5% previously.

Oil falls as traders weigh potential US–China trade talks

Oil prices fell on Friday as traders squared positions ahead of an OPEC+ meeting and amid scepticism about a potential de-escalation in the trade dispute between China and the United States.

Brent crude futures were down 23 cents, or 0.4%, at USD 61.90 a barrel at 11:05 AM GMT.

US West Texas Intermediate crude futures fell 24 cents, or 0.4%, to USD 59 a barrel.

For the week, Brent was on track for a 7% drop, while WTI was down 6.5% — the biggest weekly declines in a month.

Gold prices set for weekly drop on US–China trade talk hopes; payrolls data on tap

Gold prices rose in Asian trading on Friday as the US dollar dipped ahead of payrolls data, although gains were limited as China signalled potential trade talks with President Donald Trump’s administration.

The yellow metal suffered consecutive sharp declines over the past three days amid signs of easing trade tensions, leaving it poised to fall 2% for the week.

As of 6:53 AM GMT, spot gold rose 0.5% to USD 3,255.95 per ounce.

Gold futures expiring in June gained 1.2% to USD 3,232.24 an ounce.

Silver futures rose 1.4% to USD 32.625 an ounce.

Platinum futures climbed 0.9% to USD 982.35 an ounce.