Big moves are in play this week. With the Fed is shaking up its policy framework, and zero interest rates no longer being the default, markets are bracing for the potential ripple effects on markets, borrowing costs, and economic growth.

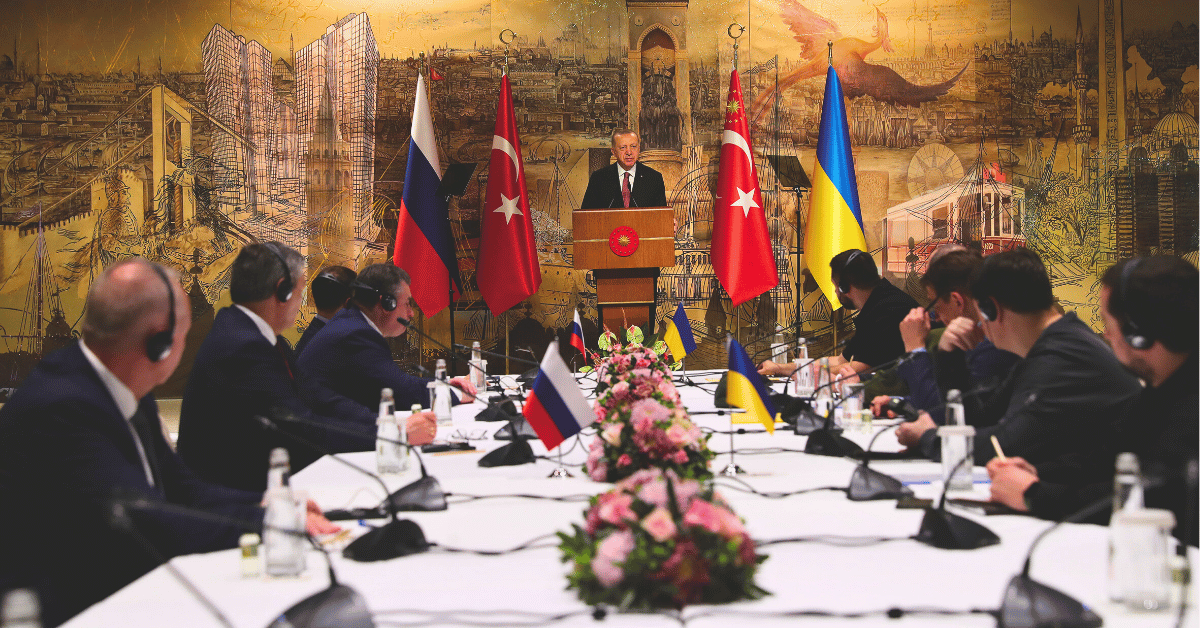

Meanwhile, the Russia-Ukraine peace talks have been pushed to May 16, but the bigger question is: Who’s showing up? Zelensky, Trump and the Kremlin, are all showing contrasting stands against one another, setting the stage for another diplomatic standoff.

In the Middle East however, Hamas signals a major shift, expressing willingness to relinquish control of Gaza if a permanent ceasefire can be secured.

As the world watches, markets react, and power players move, one thing is certain: This week will be one to watch.

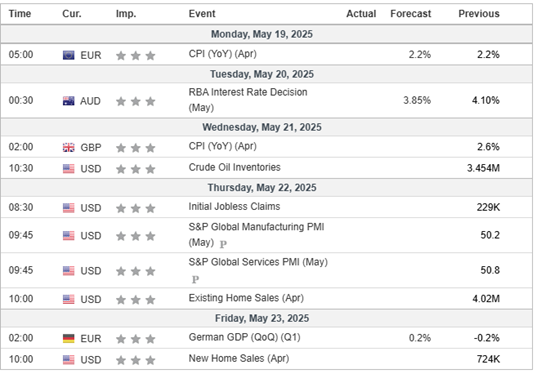

Key Economic Indicators

Monetary Policy & Fed

Fed is adjusting its overall policy framework, with zero interest rates no longer being a baseline assumption. Regulators also plan to ease leverage rules for large banks in the coming months.

Language on underemployment and average inflation to be reconsidered.

April core PCE inflation expected to fall to 2.2%.

Trade & Tariffs

Japan seeks third round of U.S.-Japan trade talks next week.

U.S. considering modifications to the current U.S.-Japan trade agreement.

EU to accelerate trade talks with the U.S.; aims for deeper tariff cuts than what the U.K. has received.

Russia-Ukraine Talks

Peace talks postponed to May 16.

Zelensky: a technical ceasefire deal could make meeting Putin unnecessary.

Trump: may attend talks in Turkey; says no progress until he and Putin meet.

Kremlin: Putin has no plans to attend or meet Trump.

Middle East

Hamas official: Willing to give up Gaza control if a permanent ceasefire is achieved.

Energy Market

The IEA has revised its 2025 forecasts as below:

Oil demand growth up to 740,000 barrels/day.

Supply growth up to 1.6 million barrels/day.

Crypto

Coinbase reported a data breach involving customer information, refusing a $20 million ransom from hackers.

The SEC is investigating an alleged misreporting of user numbers.

Market movers

XAUUSD

The primary trend remains firmly bullish.

Price action suggests a potential bottom is forming.

EUR/USD posted modest daily gains, though price action remained contained within the range from the prior trading day. This is an indecisive Inside Day.

Buying interest emerged during the Asian session.

On an intraday basis, price is trading between bespoke support at 1.1040 and resistance at 1.1237.

Market conditions are expected to stay mixed and volatile.

The U.S. dollar weakened against major peers following softer-than-expected producer price inflation data, with the Dollar Index slipping to 100.80.

EUR/USD edged up by 10 pips to 1.1184.

USD/JPY dropped sharply by 115 pips to 145.60, marking its third consecutive daily decline.

GBP/USD gained 44 pips, settling at 1.3303, after the U.K. reported stronger-than-expected Q1 GDP growth of 0.7% quarter-on-quarter compared to the forecast of 0.6%.

AUD/USD declined 21 pips to 0.6405.

USD/CHF lost 67 pips to 0.8351

USD/CAD dipped 24 pips to 1.3958.

What happened in the U.S. market

The stock market closed higher on Thursday:

Dow Jones gained 271 pts (+0.65%) to 42,322

S&P 500 rose 24 pts (+0.41%) to 5,916

Nasdaq 100 added 16 pts (+0.08%) to 21,335

It is important to observe that that both the S&P 500 and Nasdaq 100 have been extending their winning streak to four sessions.

However, the 10-year Treasury yield fell 8.9 bps to 4.439%, likely influenced by key economic data as below:

PPI (April): +2.4% YoY (vs 2.6% expected, 3.4% prior)

Stock market saw some overall gains, with the German index DAX up 0.72%, the French index CAC up 0.21% and the British index FTSE up 0.57%.

What happened to global commodities

With President Trump signaled a potential nuclear deal with Iran, the market speculated that there may be eased sanctions and increased oil supply entering the picture. As such:

Gold surged $62 (+1.97%) to $3,240/oz

WTI crude fell $1.53 (-2.42%) to $61.62/bbl, extending its decline