From 14 to 18 April 2025, key economic events are set to shape market dynamics. US–China trade tensions, evolving tariffs, and inflation data will drive investor sentiment. Central banks’ policy responses to these developments, along with growth forecasts, are also under scrutiny as markets adjust to potential risks and opportunities.

KEY INDICATORS

Policy developments: US–China tensions & global tariff manoeuvres

China’s 2025 National Export Control Meeting emphasised strengthening export control enforcement, improving regulations, and boosting multilateral cooperation in response to growing global complexities.

The EU softens its stance by pausing retaliatory tariffs on the US for 90 days. President Ursula von der Leyen warned, however, that strong measures—possibly targeting US tech giants—will be deployed if talks fail.

The US Treasury reports March net tariff revenue at USD 8.2 billion, the highest since September 2022, driven by recent tariff hikes.

The EU and China begin negotiations on setting a minimum price for Chinese electric vehicles (EVs), potentially replacing previously imposed EU tariffs.

Macro data: Inflation, budget, and policy signals

US inflation unexpectedly cools: March CPI fell 0.1% month-on-month (first drop since May 2020), while core CPI rose 2.8% year-on-year—the smallest gain since March 2021.

The federal budget deficit shrinks to USD 161 billion in March, down 32% year-on-year, driven by a calendar adjustment in spending and rising tax revenues.

Markets are now pricing in 100 basis points of Fed rate cuts in 2025, but Fed officials remain cautious amid inflation uncertainty and trade-related risks.

Germany slashes its 2025 GDP growth forecast from 0.8% to 0.1%, citing trade policy impacts and weak domestic demand.

The EIA cuts its global oil demand forecast and oil price outlook: Brent crude is now expected to average USD 67.87 per barrel in 2025, down from USD 74.22.

Market reaction & capital flows: Risk-off sentiment returns

US equities retreat as trade tensions weigh heavily on sentiment despite temporary tariff postponements.

Emerging markets see a USD 17.1 billion capital outflow in March, the largest since August 2023, driven by tariff fears and global uncertainty.

The RMB exchange rate remains flexible, with SAFE highlighting China’s resilient FX market and capacity for self-correction.

BoE and RBA officials express uncertainty over the full impact of US tariffs on domestic inflation and monetary policy paths.

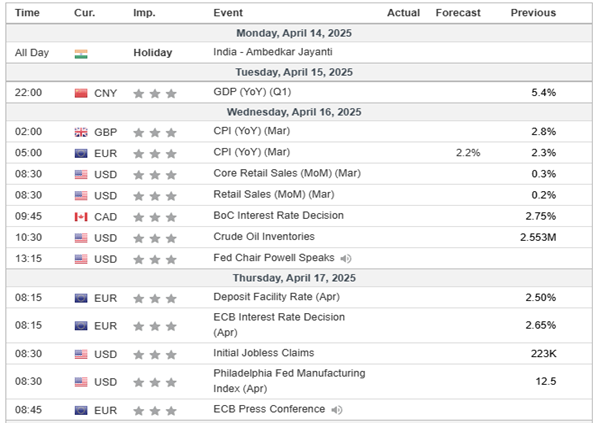

MARKET MOVERS

EUR/USD

The pair extended its upward momentum from 1.0913, closing with solid net gains yesterday.

The previous resistance level at 1.1214 has been decisively breached.

A corrective pattern has emerged on the intraday chart, signalling potential short-term exhaustion.

Current price action is trading in overbought territory.

Selling into rallies presents a favourable risk/reward opportunity.

US dollar drops sharply, safe-haven currencies gain

US dollar saw a sharp sell-off, with the Dollar Index dropping 1.92 points (-1.87%) to 100.98, marking its largest single-day decline since 2022.

Safe-haven currencies, Japanese yen and Swiss franc, extended their gains against the greenback.

USD/JPY fell 333 pips (-2.26%) to 144.44.

USD/CHF dropped 339 pips (-3.96%) to 0.8237, its lowest level in a decade.

EUR/USD rose 251 pips (+2.30%) to 1.1200.

GBP/USD climbed 140 pips (+1.09%) to 1.2954.

AUD/USD advanced 68 pips (+1.11%) to 0.6219.

USD/CAD slipped 93 pips to 1.3991.

US equities retreat as tech stocks lead the decline

US equities surrendered some of Wednesday’s gains, with the Dow Jones Industrial Average falling 1,014 points (-2.50%) to 39,593, S&P 500 dropping 188 points (-3.46%) to 5,268, and Nasdaq 100 losing 801 points (-4.19%) to close at 18,343.

US inflation slowed to 2.4% YoY in March, down from 2.8% in February, but failed to sustain bullish momentum.

The 10-year Treasury yield edged higher by 2.9 basis points to 4.425%.

Mega-cap tech stocks retreated: Tesla (TSLA) -7.27%, Meta Platforms (META) -6.74%, Nvidia (NVDA) -5.91%, Apple (AAPL) -4.24%.

US Steel (X) plunged 9.46% after Donald Trump opposed its proposed sale to a Japanese buyer.

Ford Motor (F) declined 3.79% after Goldman Sachs downgraded its rating to “Neutral.”

Cruise-line stocks hit hard after Morgan Stanley cut price targets: Carnival (CCL) -10.25%, Norwegian Cruise Line (NCLH) -9.24%, Royal Caribbean (RCL) -8.11%.

European markets rebounded strongly from prior losses: DAX 40 +4.53%, CAC 40 +3.83%, FTSE 100 +3.04%.

Commodities mixed: WTI crude oil fell USD 2.28 (-3.66%) to USD 60.07 per barrel, and gold surged over 3% to reach a record high of USD 3,176.

Gold extends rally while USD/JPY weakens in Asian session