As we approach the week of 7 to 11 April 2025, several key developments are poised to influence global financial markets. Market participants are closely monitoring President Trump’s tariff policies and their potential economic implications, as well as upcoming economic data and earnings reports. These events could significantly shape investor sentiment and market trends in the short term.

KEY INDICATORS

Trump’s tariff policy and market impact

2 April: President Trump declared a national emergency over the US trade deficit, invoking the IEEPA and introducing a two-tier tariff system.

5 April: A 10% baseline tariff will take effect on all imports at 12:01 a.m. EDT.

9 April: Additional “reciprocal” tariffs will target countries with large trade surpluses with the US.

Global markets reacted negatively, with sharp declines in Asian equities reflecting investor concerns over trade disruptions.

Economists warned that tariffs could push inflation above 4%, straining household budgets and dampening consumer spending.

The policy risks triggering a global trade conflict, with affected countries considering retaliatory measures that may destabilise international trade relations.

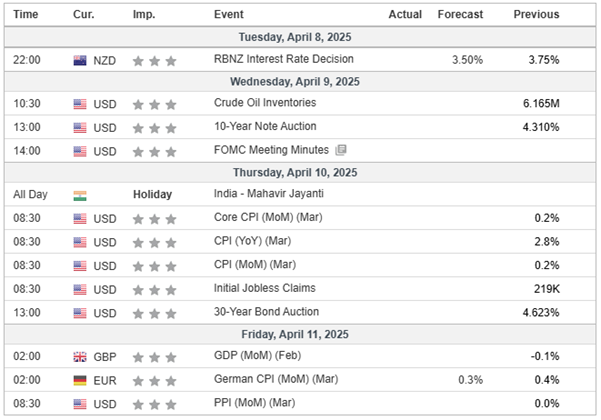

Key US economic data releases

10 April: Consumer Price Index (CPI) for March will track changes in consumer-level inflation.

11 April: Producer Price Index (PPI) for March will reflect trends in wholesale pricing.

11 April: Preliminary Consumer Sentiment Index for April will gauge public confidence in the economic outlook.

Earnings season and Fed update

7 April: Dave & Buster’s (PLAY) is expected to report earnings per share (EPS) of USD 0.66 on USD 547.99 million in revenue, marking an 8.5% year-on-year decline.

7 April: Levi Strauss (LEVI) is projected to post EPS of USD 0.28 on USD 1.54 billion in revenue, reflecting a 1.1% year-on-year decrease.

7 April: Greenbrier Companies (GBX) is scheduled to announce its earnings; details are yet to be disclosed.

9 April: The Federal Reserve will release the minutes from its March FOMC meeting, providing insight into its economic outlook and potential policy direction.

10 April: JPMorgan Chase (JPM) is expected to report continued growth, following a 21% increase in adjusted profit and an 11% rise in revenue in the previous quarter.

10 April: Wells Fargo (WFC) is anticipated to provide an update on its financial performance amid evolving economic conditions.

MARKET MOVERS

XAU/USD

The primary trend remains bullish.

We anticipate a temporary pullback.

Any setbacks should be contained around yesterday’s low.

The US Dollar Index fell by 1.69%, closing at 101.94, reflecting investor concerns over the tariff announcement.

The 10-year US Treasury yield dropped below 4% for the first time since October, closing at 4.0620%, while the 2-year yield dropped to 3.7490%.

Spot gold fluctuated wildly with a daily range exceeding USD 110, closing down 0.76% at USD 3114.28 per ounce.

Spot silver closed down 6.11%, at USD 31.82 per ounce, amid market volatility.

WTI crude oil fell by 5.8%, closing at USD 66.56 per barrel, and Brent crude dropped 4.79%, closing at USD 69.81 per barrel due to the tariffs and OPEC+ production increases.

Stock market performance: US & global declines

The Nasdaq dropped 5.97%, its largest single-day loss since March 2020, while the S&P 500 fell by 4.84%, and the Dow Jones dropped 3.98%.

The Philadelphia Semiconductor Index fell by 9.88%, and the KBW Bank Index dropped by 9.86%, its biggest decline since the regional banking crisis.

Major tech stocks were all down: Apple fell over 9%, Amazon and Meta lost over 8%, Nvidia dropped over 7%, and Tesla fell over 5%.

European stocks saw broad declines: the DAX30 dropped 3.08%, the FTSE 100 fell 1.55%, and the Euro Stoxx 50 dropped 3.6%.

Hong Kong stocks opened sharply lower with the Hang Seng Index dropping 1.52% and the Tech Index falling 2.09%, although both indices recovered slightly towards the close.

Chinese A-shares market & broader economic impact

The Shanghai Composite fell 0.24%, the Shenzhen Component dropped 1.4%, and the ChiNext Index declined 1.86%.

Agricultural and logistics stocks showed strength, while automotive and industrial equipment sectors underperformed, reflecting global trade uncertainties.